Rates are a property tax that are made up of part uniform or fixed charges for the property, and part as a rate in the dollar based on the value of your property.

Changes for 2024/25 rates year

This year Council will collect $96.8m in rates (incl GST). How much you pay depends on:

- The valuation of the property.

- The number of separate parts on a property such as multiple dwellings.

- The number of service connections for wastewater, water and refuse.

- Increases in some fixed service related targeted rates that apply to some properties.

- Eligibility for rate relief/ remissions.

There are increases in fixed rates for the Uniform annual general charge (UAGC) and services such as reticulation of wastewater and water supply. The targeted rating system means those that receive a service can expect to pay more. City residents have more reticulated services than elsewhere in the community.

In rural areas increase in rates have been driven mostly by unsubsidised roading and resource consents.

What your rates pay for

On the back of your instalment 1 rates notice is your property's rates assessment. This show details of each activity. The activities that you contribute to will vary depending where your property is in the district.

These are charged in proportion to the capital value of your property. General rates are paid by all ratepayers.

Environmental policy

The cost of advising the public on how regulatory requirements affect them and their proposals for the use of the land. The cost of the District Plan and other planning projects and reserve management plans. Also includes the cost of resource consent monitoring and RMA enforcement.

Rivers and coastal management

The cost of monitoring rivers and surface water on land and the provision of flood control works by control of vegetation on river channels, Wainui Beach erosion management scheme maintenance and preventative maintenance over the whole district.

Stormwater drainage

Contributes towards the cost of collection and disposal of rainwater. The majority of stormwater costs are paid by targeted rates in Gisborne city and rural towns. Previously 20% of the activity was funded in the general rates. This has reduced to 10% bringing it in line with wastewater and water (3 waters infrastructure).

Treasury

The cost of administering our bank accounts, loans and investments and district loan expenses. Councils have always funded some capital works by loan and this item covers the interest charges.

Economic development and tourism

Funds a portion of the economic development activity including tourism.

Planning

The cost to comply with statutory provisions of the LGA 2002, Resource Management Act 1991 and Reserves Management Act 1997. Also includes the cost of preparing, maintaining and implementing strategies, policies and plans to promote sustainable management of natural and physical resources.

Animal and plant pest management

A regional council responsibility to keep nuisance pests and noxious plants under control. All properties contribute 60% of this cost.

Waste management and waste minimisation

For solid waste legacy debt and after care provisions and waste minimisation encourages waste reduction.

Water supply

10% of the water activity is collected in the general rates as there is a wider benefit provided to the whole community by the delivery of water infrastructure. These benefits relate to improving and maintaining water quality, protecting waterbodies and coastal waters that have important ecosystem, recreational and cultural values and moving toward more efficient and sustainable use of freshwater. Most of the water activity is paid in targeted rates by users connected to the reticulation network.

Wastewater

10% of the wastewater activity is collected across the district in the general rate. There's a wider benefit provided to the whole community by the delivery of the wastewater infrastructure. These benefits relate to improving and maintaining water quality, protecting waterbodies and coastal waters that have important ecosystem, recreational and cultural values and moving toward more efficient and sustainable use of freshwater. Most of the wastewater activity is paid in targeted rates by users connected to the reticulation network.

These are charges for services or facilities which you are invoiced only if you live in the area where these rates apply or you receive benefit. These are paid by a specific group of ratepayers who receive or benefit from a specific service or activity.

Rates which can fund a particular activity or group of activities and can apply to certain areas, categories or to certain ratepayers.

The matters and categories used to define categories of rateable land and calculate liability for targeted rates are set out in the Local Government (Rating) Act 2002 Schedule 2 and Schedule 3.

Aquatic and recreation facilities rate - The cost of maintaining the Kiwa Pool complex and our recreational facilities is based on the properties capital value. Properties in the Inner Zone contribute at a weighting of 1.0 and the Outer Zone contribute less with a weighting of 0.3.

Animal control rate - The cost of minimising danger, distress and nuisance caused by stray dogs and controlling stock on roads. This is a uniform targeted rate on residential properties throughout the district.

Building services rate - The cost of providing advice to the public on regulatory requirements with the Building Act and cost of resolving complaints about building related issues including stormwater on private property based on a properties capital value. Residential and lifestyle properties in Gisborne city and on the Poverty Bay Flats contribute 85%. The remaining 15% is paid by rural properties.

Business area patrols in CBD rate - The cost of providing security in the CBD and operating CCTV security cameras for crime prevention as set out on the map at the end of this section. This is based on capital value in the CBD.

Commercial recycling rate - A targeted rate on non-residential properties within Gisborne city on each separately used or inhabited part of a property which elect to receive the recycling collection service.

Cyclone recovery rate - woody debris- A targeted rate to cover maintenance and preemptive work to protect Council assets. The targeted rate share is apportioned on capital value between the forestry sector (70%) and the pastoral sector (15%). Where 20ha or more of the property is planted in forestry, that portion will be rated as forestry. Where 20ha or more of the property is pastoral, that portion will be rated as pastoral. The remaining 15% public good component is collected from the Uniform Annual General Charge.

Drainage rates - The cost of providing land drainage in the designated areas of benefit. There are 2 groups - direct beneficiaries and contributors. Both rates are based on the area of land receiving the benefit. Maps of the drainage areas are at the end of this section.

Economic development and tourism rate - The costs of preparing for and supporting economic and tourism activity throughout the

district. This rate is payable by all industrial and commercial properties over the whole district based on capital value.

Flood control schemes rate - This is the cost of operating flood protection works. General rates fund 60% and the balance is targeted collection from those who receive benefit from the scheme in the City and Poverty Bay flats. Maps of the Flood Control Schemes are available in the policy document.

- Waipaoa there are 6 classes of the scheme from A-F.

- Te Karaka – the targeted rates are split between residential and non-residential properties.

Noise control rate - This is the cost of responding to noise complaints. This is uniform targeted rate to residential properties in Gisborne city, Makaraka, Wainui and lifestyle properties on the Poverty Bay Flats.

Non-subsidised road rate - This is the cost of non-subsidised road works in the district. This is a differential targeted rate on the Inner Zone and Outer zone based on capital value.

Passenger transport rate - This is a uniform targeted rate for providing a subsidised passenger transport service payable on residential properties per separately used or inhabited part of a property in Gisborne city.

Parks and reserves rate - The cost of maintaining all the parks, reserves, playing fields, beach access points. This is a fixed amount per rating unit. The Inner Zone contributes 85% of costs and Outer Zone 15%.

Plant and animal pests rate - To keep nuisance pests and noxious plants under control. All properties contribute, but farms pay a larger contribution. The inner zone contributes 20% and the outer zone contributes 80%. This is rated on land value.

Resource consents rate - The focus is to allocate the use of natural resources to consent holders and to protect the quality of the natural and physical environment and to provide assistance and clarity to the public. This is rated on Land value.

Roading flood damage and emergency and subsidised local roads rate - Roading maintenance and repair costs are partly fund by

Waka Kotahi (NZTA). The rate targeted portion is based on capital value and is split into differential rating groups that are weighted

as follows: Residential, lifestyle and other properties 1.0; Horticulture and Pastoral farming 1.5; Industrial and Commercial 2.0; Forestry 13.75. The remaining portion is collected as part of the Uniform Annual General Charge.

Subsidised roading rate - residential lifestyle and other properties - This is a general sector that includes residential, lifestyle, arable, utilities network and other properties that do not fall into the horticulture, pastoral, commercial, industrial and forestry sectors. A horticultural or pastoral property that is less than 5 hectares (ha) is rated in this sector. This is rated on capital value.

Subsidised roading rate - horticulture properties - Have horticulture use and are 5 hectares (ha) or greater in area. This is rated on capital value .

Subsidised roading rate - pastoral properties - Have pastoral use and are 5ha or greater in area. Where 20ha or more of the

property is planted in forestry, that portion will be rated with the weighting for forestry roading rates. This is rated on capital value.

Subsidised roading rate - forestry exotic properties - Have a forestry use. Where 20ha or more of the property is pastoral, that portion will be rated with the weighting for pastoral roading rates. This is rated on capital value.

Subsidised roading rate - commercial and industrial properties - Have a commercial and industrial and utilities use other than where it is a utilities network.

Flood damage and emergency works rate - This rate covers approximately 25% of cost of repairs to roading network from an

adverse event. The remaining balance is funded by a NZTA Waka Kotahi subsidy. Properties are rated on capital value using the weightings of 1.0 for residential properties, 1.5 for horticulture and pastoral properties, 2.0 for commercial and industrial properties and 13.75 for forestry properties. Where 20ha or more of the property is either pastoral or forestry, that portion will be rated with the

corresponding weighting (pastoral 1.5, forestry 13.75). This is rated on capital value.

Rural transfer stations rate - Partially covers the cost of operating 8 transfer stations at Tolaga Bay, Tokomaru Bay, Te Puia Springs,

Tikitiki, Waiapū, Te Karaka, Whatatūtū and Matawai. This includes the cost of cartage to Waiapū Landfill or Gisborne city.

Residential properties within a 15km radius of a rural transfer station contribute to this rate per separately used or inhabited part of a

property eg If a property has multiple dwellings, the rate will be charged per dwelling. Refuse stickers are issued to use when taking refuse to a transfer station. Ruatōria township have both kerbside collection and the use of the transfer station. A charge is payable for each service.

Soil conservation rate - advocacy and land use – This rate is concerned with erosion, land stabilisation and the effective use of land and the advice, communication and enforcement of this legislation. The soil conservation rates are split between DRA1, DRA1A and DRA2 -40%, DRA3 and DRAS4 30%, and DRA5 30%. This is based on land value.

Stormwater and drains rate - This is for the cost of stormwater reticulation to dispose of rainwater and maintain assets in Gisborne city and rural townships. Funded by a charge per separately used or inhabited part payable by residents living in Gisborne city, Wainui, Okitu and rural towns including Pātūtahi and Manūtukē. The basis for stormwater and drains on commercial properties is capital value.

Theatres rate - This is for the cost of maintaining theatres in the district. Some costs are part funded by fees and charges and part

funded by a targeted rate on capital value in the Inner zone and the Outer zone.

Water conservation rate - This is the cost of monitoring the quality and volume of natural water, and ensuring that we are using these water resources wisely and is based on land value.

Waiapū River erosion control scheme rate - Covers the operating costs and loan repayments of protection works on the river. This activity is partially (60%) funded by the general rate with the balance split between: direct beneficiaries in Ruatōria Township and around the river pay 60% of the cost of the activity balance on capital value indirect beneficiaries inside the catchment area pay 15% of

the cost of the activity balance on capital value contributors at the edges of the catchment pay 15% of the activity balance based on rate on the dollar per hectare.

Wastewater rate - 10% of costs are funded in the general rate with the balance paid by a pan charge rate to connected users.

Wastewater (pan charge) rate - A usage charge based on the number of toilet pans and urinals connected. A residential dwelling

pays only one pan charge, no matter how many toilet pans are installed. All other properties pay one pan charge for each toilet

pan or urinal installed and connected. this includes but is not limited to commercial properties, schools and hospitals.

Waste management charge rate - Solid waste / household refuse collection including the cost of recycling where the service is

provided throughout the district. This is a uniform amount for each separately used or inhabited part of a property.

Water rate

- Uniform water charge is the cost of delivering drinking water where the service is provided, payable per separately used or inhabited part of a property, for example if there are 3 flats on the property there will be 3 water charges.

- Availability charge - the charge if you are in an area where water service is supplied, but the property is not connected.

- Fixed water by meter rate per cubic metre to properties identified as an extra-ordinary use and some rural domestic users as defined in the Water Supply Bylaw 2015. Metered domestic users receive a free of charge allowance of 300 cubic metres per annum.

Lump sum contributions will not be invited in respect of the targeted rates.

This is a fixed charge per separately used or inhabited part of a rating unit (SUIP). The UAGC covers rates on activities that benefit the community equally. If you have 2 flats or dwellings on your property, you will pay 2 UAGCs.

The UAGC is $1070.75 GST inclusive, and is made up of the following rates:

| Cemeteries | $26.35 | a large proportion of the costs of running the main cemeteries are covered by burial fees. This rate covers the shortfall which cannot be recovered |

|---|---|---|

| Civil Defence | $50.50 | a statutory requirement which applies equally to all parts of the district. |

| District civil and corporate expenses | $35.96 | funds scholarships, awards, grants, civic functions, naval visits, Anzac day, citizenship ceremonies. Corporate expenses include the costs of membership of Local Government New Zealand, NZ sister cities. |

| Economic development and tourism | $4.16 | covers the costs of preparing for and supporting economic and tourism activity throughout the district. This is partially funded by a targeted rate. |

| Environmental and public health protection | $87.95 | the cost of monitoring environmental health and all other legislative activities delegated to council by central government |

| Library | $122.80 | HB Williams Memorial Library and all the rural and mobile libraries throughout the district |

| Litterbins and cleaning public areas | $12.44 | |

| Managing solid waste and transfer stations | $109.60 | the cost of operating district transfer stations and landfills, and the cost of transportation of solid waste out of the district. |

| Mayor and councillor representation costs | $146.64 | democratic process, the cost of the mayor and councillors who meet and represent the people. It also includes an allocation of the salary costs of those staff that support the council meetings. |

| Public toilets | $99.95 | cost of cleaning and maintaining 70 public toilets throughout the district. |

| Roading | $139 | contribution for maintenance and repairs to district-wide local roads. |

| Strategic planning and engagement | $97.66 | to facilitate liaison activities throughout the district including consultation specific to Treaty and Resource Management Act issues. To provide community consultation in compliance with the Local Government Act 2002. Provision of policy development as required by legislation. |

| Tairāwhiti museum | $43.31 | grant funding to Tairāwhiti museum |

| Cyclone recovery general and woody debris | 95.04 | |

| $1070.75 |

A separately used or inhabited part of a rating unit includes any portion inhabited or used by the owner / a person other than the owner, and who has the right to use or inhabit that portion by virtue of a tenancy, lease, licence, or other agreement.

This definition includes separately used parts, whether or not actually occupied at any particular time, which are provided by the owner for rental (or other form of occupation) on an occasional or long-term basis by someone other than the owner.

Interpretation rules

Each separate shop or business activity on a rating unit is a separate use, for which a separate UAGC is payable. (See Guidance Note 1.)

Each dwelling, flat, or additional rentable unit (attached or not attached) on a residential property which is let for a substantial part of the year to persons other than immediate family members is a separately inhabited part of a property, and separate UAGCs are payable. (See Guidance Note 2.)

- Each residential rating unit which has, in addition to a family dwelling unit, one or more non residential uses (ie home occupation units) will be charged an extra UAGC for each additional use. (See Guidance Note 3.)

- Each non-residential activity which has, in addition to its business or commercial function, co-sited residential units which are not a prerequisite part of the business or commercial function, will pay additional UAGCs for each residential unit. (See Guidance Note 4.)

- Individually tenanted flats, including retirement units, apartments and town houses (attached or not attached) or multiple dwellings on Māori freehold land are separately inhabited parts, and will each pay a separate UAGC. (See Note 5.)

- Each title on a multiple-managed forestry holding (that is, where the forest is broken into several individual small titles) is a separately used part except when one or more titles are adjacent and under the same ownership, in which case the rules of contiguity apply.

- Each block of land for which a separate title has been issued is liable to pay a UAGC, even if that land is vacant. NOTE: for the purpose of this definition, vacant land and vacant premises offered or intended for use or habitation by a person other than the owner and usually used as such are defined as used. Two or more adjacent blocks of vacant land are not eligible for Remission under "Contiguity" (S.20 of LG(R)A 02) because they are not "used for the same purpose" (i.e. they are not used at all).

- Each dwelling, flat, or additional rentable unit (attached or not attached) on a pastoral, horticultural or forestry property which is let for a substantial part of the year to persons other than immediate family members is a separately inhabited part of a property, and separate UAGCs are payable.

- For the avoidance of doubt, a rating unit that has a single use or occupation is treated as having one separately used or inhabited part.

- A substantial part of the year is considered to be three months or more (this total period may be fragmented, and may occur at any part of the rating year).

Guidance notes

The following notes are not rules, but are intended to aid officers in the interpretation of the rules.

Commercial properties

- A single building on one title with 24 separate shops would pay 24 UAGCs.

- A motel with an attached dwelling would pay only one UAGC, because the attached dwelling is essential to the running of the motel. (See rule D above).

- A motel with an attached restaurant which is available to the wider public has two separately used parts, and would pay two UAGCs. Likewise, a motel with an attached Conference Facility would pay an additional UAGC.

- A business which makes part of its income through the leasing of part of its space to semi-passive uses such as billboards, or money machines, is not regarded as having a separately used or inhabited part, and would not be charged a separate UAGC.

- For the avoidance of doubt, an apartment block in which each apartment is on a separately owned title is merely a series of co-sited Rating Units, and each will pay a UAGC.

- If, however, in the above example a management company leases the individual titles for 10 years or more, and those leases are registered on the titles, and the leases stipulate that the management company is responsible for paying the rates, and if the management company then operates the apartments as a single business operation, that business operation may be considered for a remission under Council's remission policies and have all but one UAGC remitted.

- An apartment block with separate laundry, or restaurant, which are available to the general population as a separate business enterprise, would pay an additional UAGC for each of these functions as separately used parts.

Residential properties

- The rule will apply to properties identified as "flats" on the valuation record, administered by Council's valuer. Sleep-outs and granny flats will generally be identified as "sleep-out" on the valuation record and will not normally qualify for additional UAGCs.

- If a property is identified on the valuation record as having flats, but these in fact are used only for family members or for others for very short periods, then the additional UAGCs may be remitted on Council receiving proof of their use, including a signed declaration from the property owner (see remission policies). A property owner who actively advertises the flats for accommodation will not qualify for the remission.

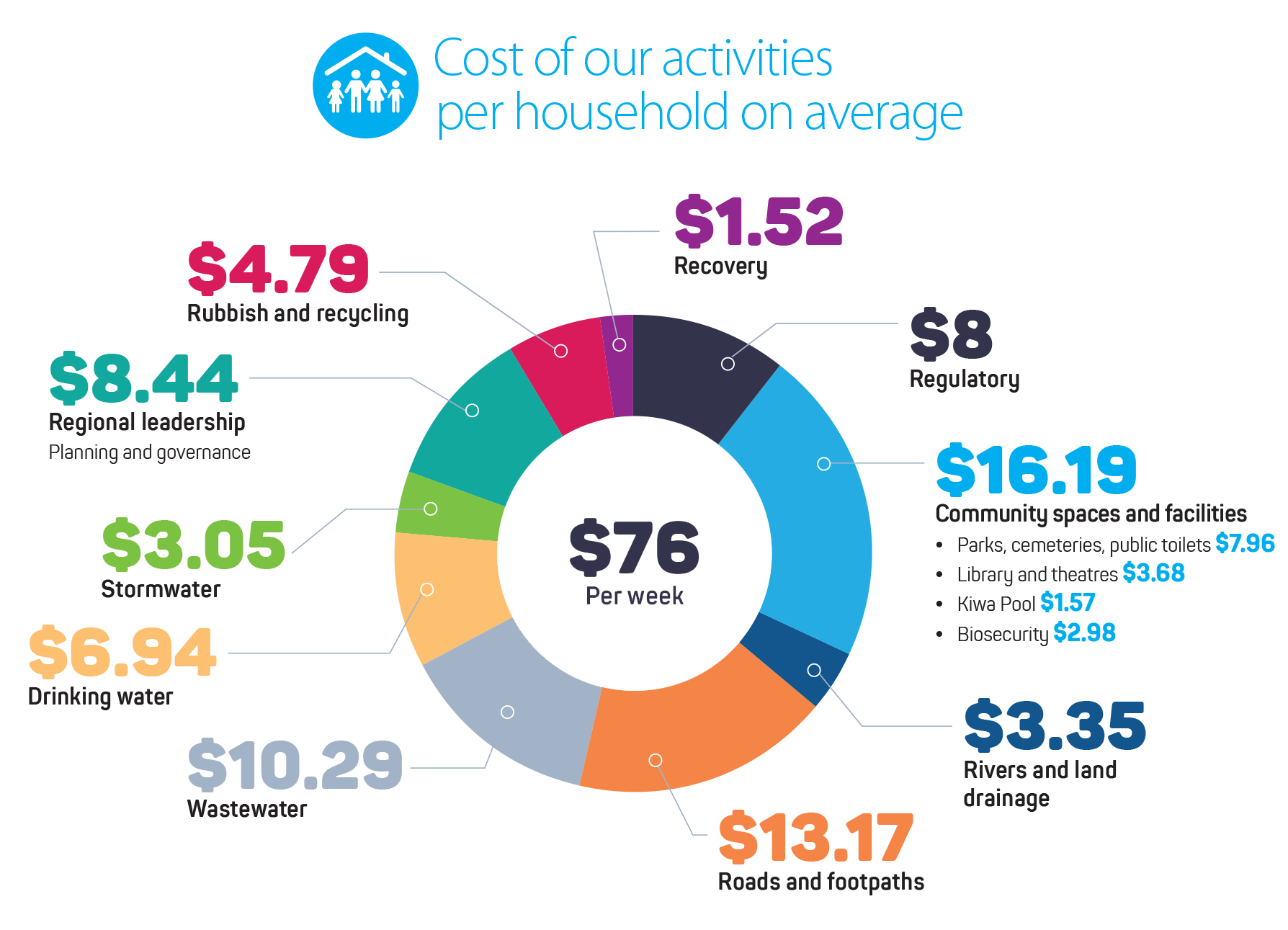

Estimated cost of activities a week per household on average